Tax credits in the U. S. U.

S.

Introduction. Renewable energy is playing an

increasingly significant role in the U. S.

In the U. S. PTC ; a credit based on the amount of energy

delivered once a facility is operating).

Wind energy has received tax credits, much in the form of PTCs. In the recent decade the U. S. Congress

allowed credits to lapse, and then reinstated them, in an arresting pattern of

fits and starts. This is shown for wind

energy in the following graphic:

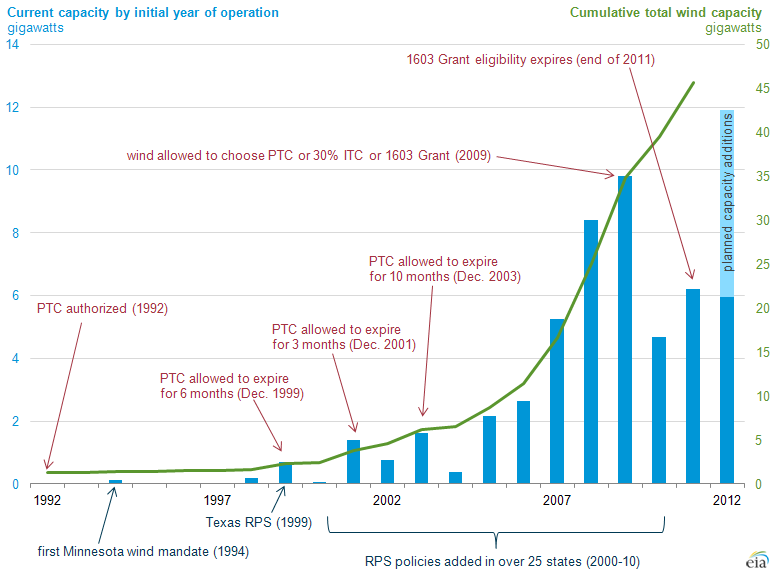

{kind=link}

History

of ITCs and PTCs for wind energy in the U. S. The blue

bars show annual wind generating capacity added each year, using the scale

for gigawatts added shown on the left vertical axis. The light blue section of the bar for 2012

shows planned capacity additions at the time this report was prepared late in

2012, presumably in anticipation of the expiration of the PTC at the end of 2012. The green line

shows the total wind capacity installed in the U. S.

Source: U. S. Energy

Information Agency; http://www.eia.gov/todayinenergy/images/2012.11.21/windcaplarge.png.

It is quite clear

from this graphic that periodic expiration of tax credits (see the years

following expirations in 1999, 2001, 2003, and 2009) had drastic negative

impacts on installation of new generating capacity during the following

year. In addition, as noted in the

legend to the graphic, during 2012 wind industry planners were factoring in a

scheduled termination of the PTC

effective at the end of the year by accelerating new construction.

Extension of

Renewable Energy Tax Credits. The so-called “fiscal cliff” in the U. S. Jan. 1, 2013 . At

literally the last minute, in an effort to avoid this fiscal crisis, the U. S.

Congress passed the American Taxpayer Relief Act of 2012 (the “Act”) on Jan. 1,

2013, and President Obama signed it into law on Jan. 3.

In addition to

provisions averting many facets of the looming fiscal disaster, the Act

included provisions extending tax credits for renewable energy.

Renewable Energy

Provisions of the Act. The Act provides extensions of tax credits with

slightly more favorable terms than in previous years. Most of the provisions are summarized here.

a)

A

production tax credit or an investment tax credit for wind energy is

extended for one year ending Dec. 31, 2013, but the terms are liberalized by requiring only that construction must have

begun by that date rather than, in earlier versions, been completed by

then. A total of $12 billion may benefit

the wind industry over the next 10 years;

b)

a credit

for energy efficiency in existing or new homes;

c)

a

credit for vehicle refueling facilities providing alternative fuels;

d)

a

credit for biodiesel and renewable diesel fuel mixtures, applied to

fuels sold after Dec. 31, 2011 and by Dec. 31, 2013 ;

e)

for the

four tax credits described above, the deadline is extended to Dec.

31, 2013 , but the subject

of the credit must have become available for use after Dec.

31, 2011 . Thus they are retroactive for about one year,

and expire after one year;

f)

a

credit for producing cellulosic biofuels after Dec. 31, 2008 and before

Jan. 1, 2014, applicable to a wide range of newer cellulosic sources and to

cultivated algae; thus this provision is retroactive for four years and remains

effective for one year. There is also a

special allowance for facilities that produce the newer cellulosic or algal

biofuels, placed in service after Dec. 31, 2012 and effective for one year;

and

g)

a

credit for geothermal facilities whose construction begins before Jan. 1,

2014 .

The New York Times

reports that electricity produced from other forms of renewable energy

sources, including tides and ocean waves, landfill methane and hydroelectric

facilities were also included in the tax credits.

Analysis

Extension of Tax

Credits. The American

Taxpayer Relief Act of 2012 included several provisions extending PTCs or ITCs

for the relatively short period of 1 year, as itemized in this post. This 1-year extension contributes, albeit

only briefly, to helping wind energy and other renewable energy technologies to

provide an increased share of America U.

S.

The legislative

wrangling over whether, and how, the fiscal cliff could be averted was itself a

cliffhanger. It was not until the last

days before the fiscal cliff deadline of Jan. 1, 2013 that the outlines of the law were

assembled, and final passage required a late night session of the lower

chamber, the House of Representatives, on New Year’s Eve extending into the

early hours of the new year. Most of the

renewable energy credits were extended for only one year. Thus the Act guarantees yet another period of

uncertainty promising yet another contentious legislative struggle over further

extensions in one year’s time. Nevertheless the Act liberalized the credits

by extending them to projects whose construction will have begun before the expiration

date, replacing the earlier requirement that projects must have been completed

by the deadline date.

Policymaking by

fits and starts is highly disruptive. Governing in this way, by awarding and

withdrawing tax benefits literally at the last minute on a schedule of once a

year to once every few years, is extremely disruptive for business activity

(see the graphic above). Corporations

and entrepreneurs seeking to develop renewable energy need multi-year periods

for planning, funding, and installing renewable energy facilities. Depending on the particular technology and

location, this can include factors such as gaining zoning and siting approval,

undergoing environmental impact analysis, assembling financing, garnering

purchase contracts for the energy ultimately produced by the renewable source,

and construction. For example, according

to the American Wind Energy Association, developing a new wind farm requires

18-24 months. Many of these factors are

interdependent. Singly or in conjunction

with one another, settling these arrangements requires extended periods of

time. It is highly counterproductive for

developers to have to contend with short-term provision and expiration of tax

credits. Effective energy policy must

create long-term stability in order to enable the justified expansion of

renewable energy technologies.

It would be far

more reasonable and effective to develop policies on subsidizing the

development of renewable energy on a long-term schedule. In this way

corporations and entrepreneurs could plan the development and implementation of

projects secure that subsidy policies were intact, available as scheduled, and

could be used as appropriate throughout the lifetime of the project.

This view conforms with the history of the use of subsidies in the

Advantages of

renewable energy. Construction and development of renewable

energy projects have many positive policy features. The new facilities will

operate within the U. S.

Developing

renewable energy preserves and/or creates jobs.

The American Wind Energy Association

states that currently 75,000 workers are engaged in wind energy. It expects that the policies in the Act could

save as many as 37,000 of those jobs and create many more in later years. There are almost 500 manufacturing facilities

in the U.

S.

Renewable energy

sources have the very important feature of not emitting greenhouse gases into

the atmosphere. Global warming due to

manmade greenhouse gases is already a very serious problem and is destined to

get worse as humanity's demand for more energy grows. New fossil fuel-based

energy- facilities put into service now, such as oil and gas pipelines,

electric generating plants, oil refineries, and the like, will continue operating

for a useful lifetime of, say, 40-50 years. These new facilities will continue spewing

greenhouse gases into the atmosphere throughout their service lifetime, adding

to those already accumulated and worsening global warming. In contrast, renewable energy facilities, once

placed in service, have close to zero lifetime emissions of greenhouse gases,

yet have the potential capacity to provide a significant portion of America

The American

Taxpayer Relief Act of 2012 laudably includes a one-year extension of tax

credits for wind energy and other forms of renewable energy. It is lamented that the extension is for only

one year. This prevents entrepreneurs

and businesses from making plans for further development of renewable energy

with the certainty of having a long-term policy in place. The expanding renewable energy industry

provides jobs for American workers, contributes to freedom from reliance on

foreign sources of energy, and relieves the burden of accumulating greenhouse

gas emissions in proportion to its installed generating capacity. All efforts should be undertaken to implement

a long-term energy policy in the U. S.

Hi there! great stuff here, I'm glad that I drop by your page and found this very interesting. Thanks for posting about renewable energy tax credits. Hoping to read something like this in the future! Keep it up!

ReplyDeleteThe Investment Tax Credit (ITC) was originally part of the Revenue Act of 1962. In subsequent legislation the ITC was modified to include incentives for renewable energy property. Currently, taxpayers can choose to use the ITC in lieu of the PTC for eligible property. To be considered eligible, most renewable source property must be placed in service by December 31, 2013. However, solar and geothermal property can be eligible if placed in service by December 31, 2016.

Hi, nice post. Well what can I say is that these is an interesting and very informative topic about wind energy tax credits . Thanks for sharing your ideas, its not just entertaining but also gives your reader knowledge. Good blogs style too, Cheers!

ReplyDelete